Background

US GAAP Financial Reporting

Taxonomy was created for SEC registrants who file financial reports in

accordance with US GAAP. The taxonomy is

both broad and deep in covering financial reporting concepts, “including all US

GAAP and SEC financial statement disclosure requirements and many elements for

commonly followed reporting practices” (XBRL US, Inc., 2008). The taxonomy is maintained and updated and is

available to the public on the XBRL US, Inc website (www.xbrl.us). The taxonomy can be viewed and read by using

software available to the public.

The XBRL US GAAP Taxonomy not

only includes taxonomies to meet mandatory requirements of the core financial

statements, notes, disclosures and schedules, it also includes taxonomies to

cover such things like Management Discussion and Analysis (MD&A),

Management’s Reports on Internal Control Over Financial Reporting, Accountant’s

Report on Financial Statements, etc. (XBRL US, Inc., 2008).

Entry Point

Since there are so many

different types of companies that report using the XBRL US GAAP Taxonomy, the

taxonomy has what are called entry points.

“An entry point is an XBRL file that brings together a set of financial

concepts that have common relationships.

For example, the “insurance” entry point (ins-stm-dis-all) brings

together financial concepts that are commonly used by insurance companies and

organizes statements, disclosures, documentation, and references” (XBRL US,

Inc., 2008). Regardless of the industry

chosen, the entry point loads the same complete list of elements…the elements

are just organized specific to that industry.

The XBRL US GAAP Taxonomy

Preparers Guide explains that the taxonomy cannot account for every reporting

possibility in every type of industry.

Therefore, it suggests that if the specific industry is not an option,

choose “the entry point that most closely reflects the financial statements”

(XBRL US, Inc., 2008). The guide

continues to explain that “the Commercial and Industrial entry point, which

includes financial reporting concepts for oil and gas, and utility entities,

has the broadest coverage of the entry points and should be used as the default

if preparers are unable to determine a more appropriate industry entry point”

(XBRL US, Inc., 2008).

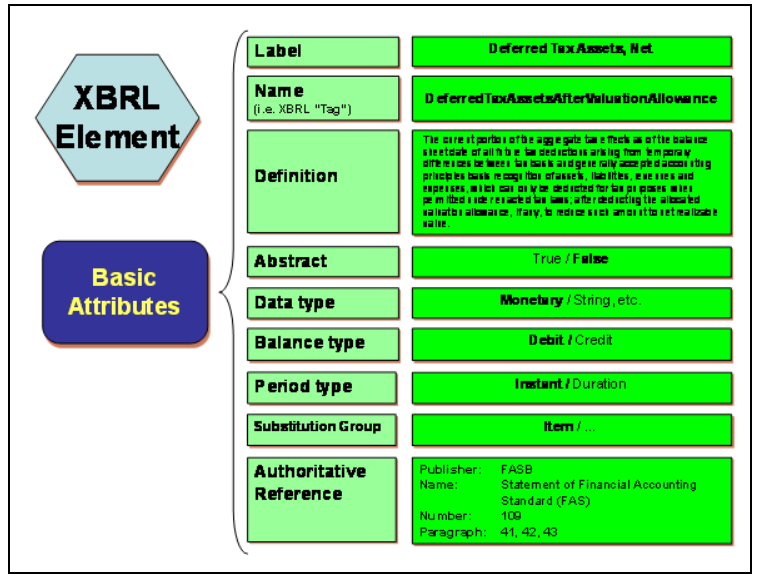

Elements

“Elements represent financial

reporting concepts that are numeric, textual (strings of text, sentences or

groups of sentences), and date-oriented” (XBRL US, Inc., 2008). There are two components of the meaning of an

element, attributes and relationships.

“Attributes are the properties that provide the defining characteristics

of a stand-alone, independent element.

Relationships are the “external” characteristics that further define the

element in terms of the other elements in the taxonomy” (XBRL US, Inc., 2008). See below for the attributes of an element

(XBRL US, Inc., 2008).

See below for an example of a

relationship (XBRL US, Inc., 2008).

Viewing and Downloading 2013 US GAAP Financial Reporting

Taxonomy

Anyone can view the taxonomy

by visiting the Financial Accounting Standards Board’s (FASB) website at www.fasb.org. The taxonomy can be viewed in its entirety or

by entry point. It can also be

downloaded to Excel. Below are some

screen captures of the public view and the Excel view (FASB, 2013).

XBRL US GAAP Taxonomy in my workplace?

As I learn more and more

about XBRL, I sit back and wonder if I’m actually getting this or just getting

more confused. There is so much to learn

about XBRL and how it can be used in the workplace, even for those that are not

required to report to the SEC. I work

for a public transportation company and I think that we could use XBRL to

streamline the reports that we are required to do to several different agencies

from Federal to State and Local. It

would be nice to be able to have the computer extract the needed information

and report it where it is needed, instead of manually retyping all the data into

each form for each report for each agency.

I look forward to the day when we can eliminate human error just due to

a typo.

References

Financial Accounting Standards Board. (2013). Entire

2013 US GAAP Financial Reporting Taxonomy. Retrieved from http://www.fasb.org/jsp/FASB/Page/SectionPage&cid=1176160582432

Gray, G., & Miller, D. (2009). XBRL: Solving

real-world problems. International Journal of Disclosure and Governance,

6(3), 207-223.

Janvrin, D., & Gyun No, W. (2012). XBRL Implementation:

A Field Investigation to Identify Research Opportunities. Journal of

Information Systems, 26(1), 169-197.

XBRL US, Inc. (2008). XBRL US GAAP Taxonomy Preparers

Guide. Retrieved from http://xbrl.us/preparersguide/Pages/frontmatter.aspx

No comments:

Post a Comment